Say Goodbye to Passive Management

Say Goodbye to Passive Management

The Volcker Era Returns.

The last decade has really been run by passive management. Indexing was the go-to strategy for many money managers and it worked.

I mean why not? You raise assets, park it in ETFs and collect our .05%-2% fee and call it a day.

Growth stocks took off and SPACs became popular trading sardines for the-day trading crowd.

But all that has ended.

Navigating economic cycles is difficult in some sense because it requires, in my opinion, two available approaches.

Stay invested and ‘ride it out’ (the preferred advisor approach)

Actively manage and adjust where capital allocations go to

Needless to say I am a believer in the latter.

Making returns in a an easy-credit/money environment for buy and hold is relatively straight-forward.

It really is. You buy quality companies with great balance sheets and can even mix in speculative growth names to give the portfolio a boost if they hit a 5/10 bagger.

But in this new era we’re embarking in it’s only going to get harder.

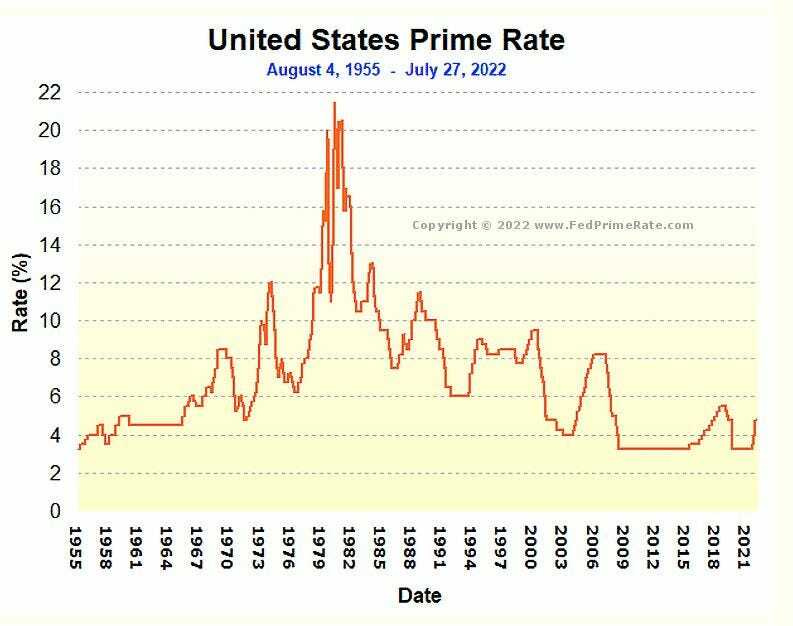

The Volcker Era, Revisited

Inflation is bad right now…the real number is probably higher than calculated and we’re in the shadow of the Volcker Era.

In 1980 inflation hit 14%. Unemployment went to 9.7% in 1982 and the market was getting crushed.

Oil traded higher (like it is now) and easy money policy ended.

The prime rate went to 21% then which, in my opinion, we won’t get to this time but we’ll get close.

Over the last few years I’ve heard the term “this is the roaring 20’s again but for our era” thrown around a lot. Money has been cheap, in fact, free with PPP loans (which arguably caused much of this) and borrowing has been cheap to fuel the economy.

We’ve had a big part for the last decade and when we though the DJ was turning off the music in late 2019 Covid came and DJ Jerome Powell decided to play another set.

But, the party is officially ended and the hangovers are coming.

Just like Volcker had to do in the 80’s the current Federal Reserve must do now. It’s going to be tough medicine to take that will cause a recession. When? Who knows but it seems to be imminent.

And maybe, like in the 80’s, we get recessions until the hangover ends.

We had one in the start of 1980 and then another that lasted 16 months from July 81 to November 82. We also had the Iranian oil embargo then which worsened economic conditions.

Today, we have something similar with an administration that is a major player in our energy problems (contrary to the gas-lighting they attempt to do).

So, while my goal is not to be Mr. bad news bears in this, it is to try to shine some clarity on an otherwise complicated topic.

Volatility will Remain

So knowing that we’re in an era similar to the early 80s with a Fed waging a battle against inflation what does that do for markets at large?

Volatility will remain a constant. This is seen as bad for most investors, especially the passive crowd.

I’ve said this in prior posts this year.

But the positive about volatility and the markets at large is that capital still flows and can produce returns.

Sure, it might not be buying growth stocks or breakouts but alpha can and should be generated in all market environments - that’s my philosophy and that likely comes from being a proprietary trader and working in the hedge fund space; if we don’t make money we don’t get paid.

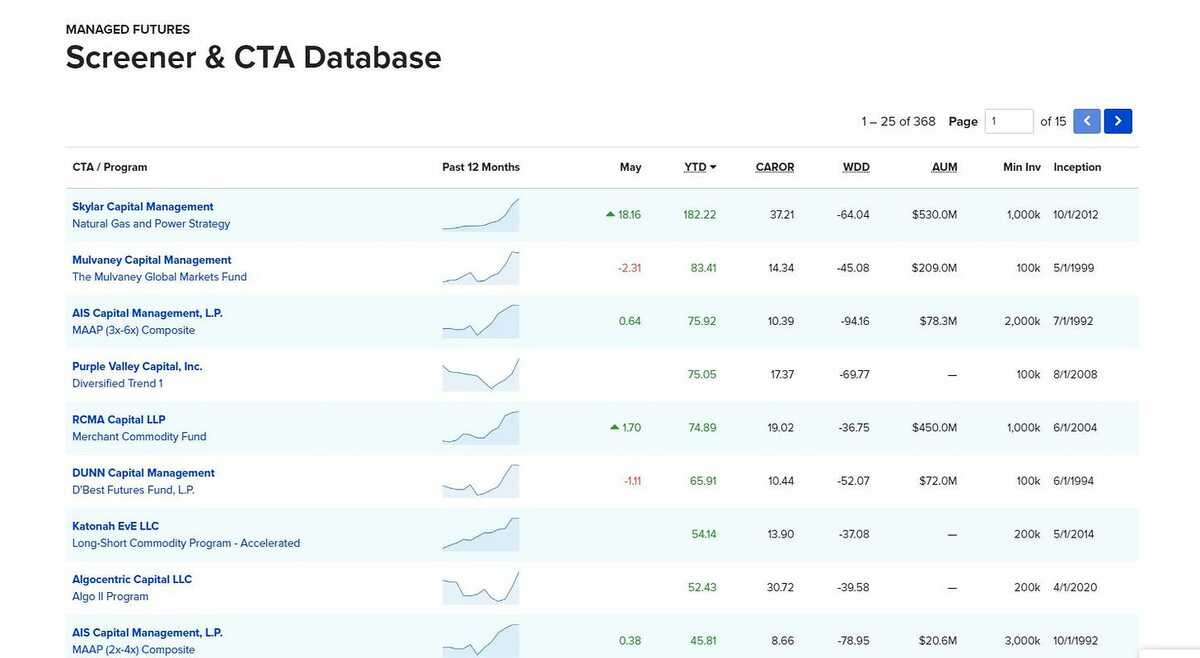

And yes while many larger hedge funds have suffered this year there are some that have thrived. There are also Commodity Trading Advisors who are the real rockstars in this era right now.

But markets at large, especially in the general money management space don’t like to discuss shorting or commodities markets too much. One, regulations make it tough for most advisors to put clients into anything but standard stocks and ETF’s because of the liability that goes on them.

Two, many of them are just not skilled to invest in those markets.

In fact, the most common question I’ve got over the years is always “what stocks do you like?”

Now, the good money managers are like great politicians; they’ll tell you what you want to hear and lie to your face.

When I’ve got that question it’s hard to answer because most of the time it’s not really a stock/company that I really like but an idea about a sector or something to do in the commodities space.

That talk is never sexy….but it drives alpha - you can see it in those returns above.

A new Approach

I don’t ever like to paint myself in a corner as a ‘type of investor’ - I really don’t. You have the Buffett value guys who get excited when they say the word ‘moat’ (company moats) then you get the types who love 200D moving averages.

My belief is that you follow the money. It always has been.

If that meant following SPACs for part of a portfolio during that short-lived hysteria then you follow it.

If that means diving into energy markets via commodities/futures then you follow it.

If that means establishing a short-book for part of the portfolio (esp. in this era) then you have to follow it.

And then….and it will be a while, when easy money comes back and Uncle Jerome does his best Volcker impersonation we can all dive back into the herd stocks.

But until that happens it’s an era of active-management.

In fact, I would go to argue that most of investing requires some element of active management, even during eras of easy money.

But today more than ever it requires it. I mean, you might not like ‘trading’ but the moves in WTI Crude oil this year during a 1-5 day period have produced alpha generating opportunities.

Now some of you are true-believers.

You’ll sit through the portfolio draw downs and say it will come back. Then there are the types who quote Warren B. on buying good companies as a way to rationalize the missed opportunities.

But think of it this way; while your invested capital is taken to the wood-shed it could have been re-allocated to different sectors and produced alpha.

So in essence it has become dead capital until The Fed decides to give the markets CPR once again.

Not for me.

Sure, I like some companies to hold for a long time but this is not 1950 anymore.

We’re in a new era of capital markets and monetary policies and if one doesn’t see or refuses to see that they’ll be left behind.

This article is presented for informational purposes only, is an opinion, and is not intended to recommend any investment, and is not an offer to sell or the solicitation of an offer to purchase an interest in any current or future investments. Any such solicitation of an offer to purchase interest will be made by a definitive private placement memorandum or other offering documents.

DIY Investor with more than $50,000? Consider joining DeltaOne.

Too Busy to Research? Check Out The TLV Report.

Thank you for reading. LongVol grows through word of mouth. Please consider sharing this post with someone who might appreciate it.